Companies in the semiconductor industry accelerated the trend towards consolidation in electronics according to A.T. Kearney’s Industrials Executive M&A Report 2019. The semiconductor industry itself obviously is also in full flux with IoT (the Internet of Things) becoming the main driver of the industry and expected to supplant wireless communications.

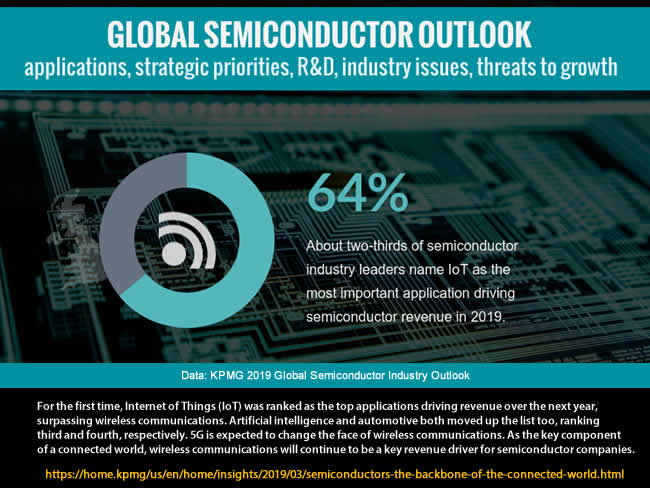

It is one of many findings from the KPMG 2019 Global Semiconductor Industry Outlook, conducted in collaboration with the Global Semiconductor Alliance and released early April 2019. While about two-thirds of the 149 leaders of semiconductor companies ranked IoT first as the main application driving semiconductor revenue in 2019, wireless communications ranks second with roundabout 60 percent of respondents.

Yet, there is another ‘application’ – or rather set of applications – that deserves attention and is driving revenue: artificial intelligence. AI / cognitive / deep learning increased from 43 percent in 2018 to 56 percent in this year’s Global Semiconductor Industry Outlook, moving up from the tenth to the third spot.

Attention: do note that driving revenue doesn’t equal providing revenue. For 2019 wireless communications (which also includes chips for mobile devices), consumer electronics, data centers/storage, industrial and automotive is the top five expected to provide the highest average percentage of company revenue.

IoT, AI and wireless communications in the semiconductor industry

It’s clear that IoT, wireless communications and AI overlap to an extent. The combination of IoT and AI is well-known by now: you don’t just want the data but also need to put them at work or simply make sense of them, for starters.

AI is also used for various areas in wireless communications and needless to say that with 5G coming our way and still quite some work ahead in cellular IoT network roll-outs (LTE-M and NB-IoT), wireless and IoT go hand in hand with “new” standards in several types of wireless IoT areas (from PAN and LAN to the wide area network protocols where we find LPWAN standards such as LTE-M and NB-IoT).

On the longer run 5G and IoT also are expected to have an important impact, among others in the industrial IoT context. However, we aren’t there at all yet. Let’s face it: even the above mentioned cellular LPWAN standards are far from omnipresent. More about 5G below.

Back to the semiconductor industry outlook. Among the reasons why the impact of AI on the industry needs to be watched isn’t just the fast-growing revenue generation from AI in the semiconductor market but also the fact that AI spurs chip innovation as the press release announcing the KPMG 2019 Global Semiconductor Industry Outlook puts it. Moreover, a lot of innovation in this space comes from smaller firms (more below).

AI offers semiconductor manufacturers an enormous opportunity, KPMG emphasizes. Or in the words of Lincoln Clark, KPMG Global Semiconductor Industry Leader: “If IoT and 5G will enable the connected world, then AI will make sense of it. AI is beginning to drive a more significant share of the semiconductor revenue stream as respondents ranked AI as the third most important application driving revenue; a significant jump from last year’s results when AI ranked tenth.”

5G’s impact on the semiconductor market and wireless communications: beginning

From tenth place to third place isn’t bad at all but, how else could it be, a lot of attention also goes to the ‘brave new world’ of 5G. It isn’t ready for IoT yet, but this year we see the first deployments and devices, even if we need to look out for hype.

Tim Zanni, KPMG Global and U.S. Technology Leader on the evolutions in 5G: “We see more concentrated local area, campus-type deployment as the first wave of 5G. This will enable use cases to be tested and new business models to be refined.” That seems like a good way to describe where we stand.

Yet, it’s clear that 5G is poised to have a serious impact on the semiconductor industry and on wireless communications overall. As KPMG puts it: “5G is expected to change the face of wireless communications. As the key component of a connected world, wireless communications will continue to be a key revenue driver for semiconductor companies.”

5G networking is one of the future drivers of the semiconductor industry as KPN has identified them, along with AI, IoT and automotive.

Challenges, issues and the road ahead for the semiconductor industry

Obviously, the KPMG 2019 Global Semiconductor Industry Outlook doesn’t just look at the technologies or applications expected to drive most revenue in the semiconductor market but also at strategic challenges in the industry with advice and findings on the way forward.

Lincoln Clark on semiconductor company challenges: “Our survey also found that demands for talent to support the innovation were mentioned as the greatest overall threat to meeting future growth. This talent risk was particularly prominent in smaller companies, while larger companies were also equally concerned about being disrupted by emerging technologies”.

Just as was the case in the A.T. Kearney survey on expected M&A activity the automotive industry also gets special attention from the semiconductor perspective. This isn’t much of a surprise since semiconductors obviously are important in automotive since many years.

However, it’s worth pointing out that while AI jumped to the third position from an expected revenue perspective, automotive climbed up to the fourth spot and remember that automotive is one of the four main future drivers for the industry as cars (and do think about anything in a context of cars, including entertainment systems and all the new phenomena we’re about to see in coming years) have become and are becoming far more than just vehicles.

Perhaps it’s also worth reminding that the automotive industry is expected to be the sector driving 5G demand, more than any other market, which is a different story.

The KPMG 2019 Global Semiconductor Industry Outlook: more findings and sources

The report further looks at topics such as node sizes, geographic differences, supply chain challenges, R&D spending and a range of issues.

They range from keeping up with diverse customer demands, the continuation of Moore’s law and scaling, high costs for fab and backend equipment, speed to market, business diversification, ecosystems and more strategic priorities and challenges for semiconductor companies over the next years. And, indeed, mergers, acquisitions and joint ventures are tackled here too. Last but not least, there is also a look at the types of semiconductors.

Some additional highlights from the KPMG 2019 Global Semiconductor Industry Outlook:

- Semiconductor industry leaders expect that the U.S. and China will remain the top revenue-generating markets over the next three years.

- Smaller companies are becoming more and more important as the source of many ‘promising developments’ in the semiconductor industry with mainly IoT and AI as their focus.

- The top three ranked as top growth opportunity sector from the perspective of types of semiconductors is 1) sensors/MEMS, 2) analog/RF/mixed signals and 3) GPUs (think, for example VR and AR, both expected to drive revenue in 2019 according to 32% of respondents).

- The main issues facing the semiconductor industry are rising R&D costs (another reason, along with the above-mentioned innovation from small firms for more M&A activities) and cross-border regulation with both issues being connected.

More information in the press release, additional findings on the overview page of the report and all findings from and advice in the KPMG 2019 Global Semiconductor Industry Outlook in the full report (PDF opens).