The main IT industry evolutions and technologies enabling digital transformation in 2018 and beyond include human-digital interfaces, artificial intelligence (AI), open API ecosystems, cloud services and infrastructure, digital trust and blockchain, data-as-a-service, DX platforms and multiplied innovation leveraging the Internet of Things, AI services and other innovation accelerators.

Originally we wanted to call this post ‘Key information technology evolutions and technologies that enable the next steps in digital transformation and the second stage of the third platform era and the crucial backdrop against which to see them and the IDC FutureScape 2018 IT predictions’. However, that seemed too long for Google. Still, now you know what it is – more or less – about.

In a previous article on digital transformation in 2018, written before the IDC FutureScape 2018 information technology evolutions predictions which we mention in this article were announced, we called upon organizations to have a far more interconnected DX approach instead of the current siloed approach which we still see in both digital transformation projects and the ways we tend to speak about the myriad technologies enabling digital transformation.

As readers of this site know we like to have an integrated, ‘holistic’ approach and emphasize the need to build bridges on several levels in a digital transformation strategy. The mix or the intersection as the quote from Forrester it in that article called it.

Obviously that precise mix depends on an organization’s context and that of the full ecosystem within which it resides. And of course it’s also about the goals that, as we know can be more immediate and provide less value or be more focused on innovation and more value. That mix, intersection or, as we tend to call it hyper-connectivity, indeed is not just about technologies and also not just about the mix of people, processes, data, purpose and what not. It’s all of that and more, including hyper-connected optimization and innovation.

A second element to take into account for the IT industry in 2018 is uncertainty. There isn’t just a changing mindset with regards to IT and the goals to achieve, there is also geo-political stability, economical uncertainty, the impact of new regulatons and more.

In this article we look at technologies first and IT industry forecasts (on a spending and risk level) next and we cover some key takeaways of the IDC FutureScape 2018 worldwide IT industry predictions IT spending forecasts from Gartner and others and the – for us key – mentioned backdrop of convergence and opportunity and uncertainty and risks against which they are, well, predicted. As you’ll see it has a lot to do with the things we’ve just mentioned.

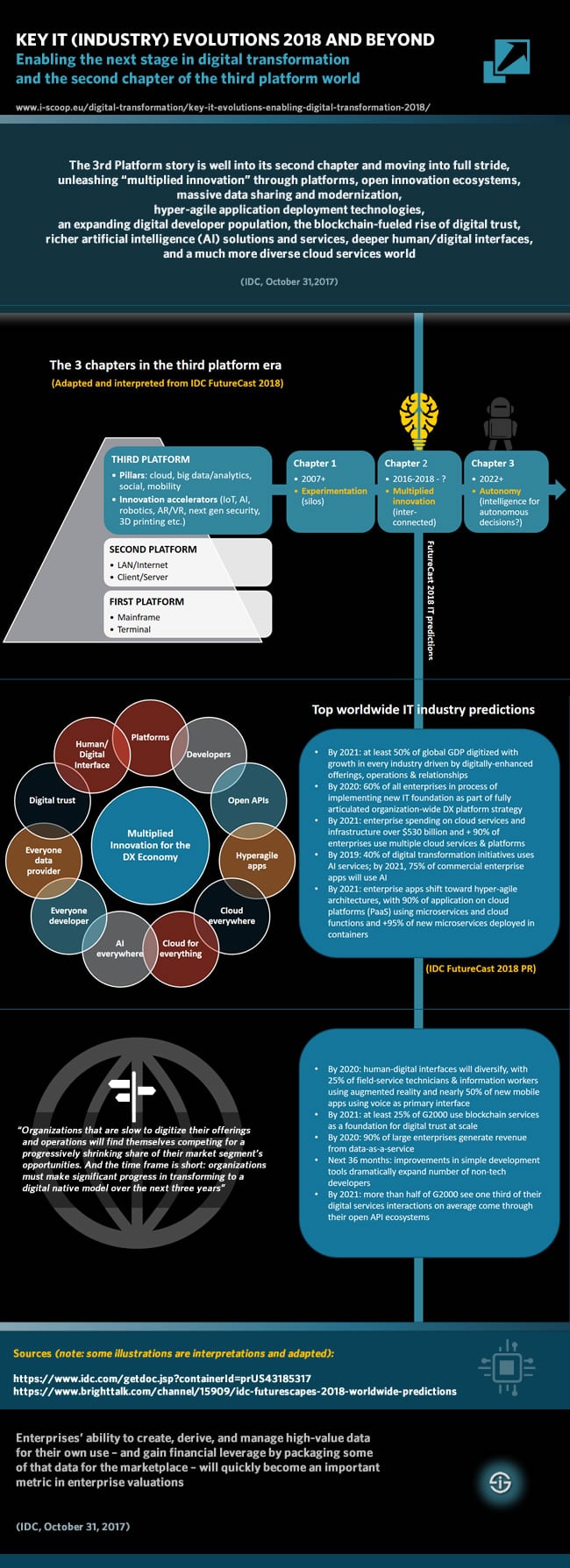

Disconnected systems and data silos- the first chapter of the third platform era

Let’s take that hyper-connectivity a step further on the IT level. Because it’s also about how various technologies interact and are leveraged in combined forms in order to realize the digital transformation and business goals as such.

It’s as we wrote in a piece on the evolutions on public cloud services evolutions recently: cloud and IoT, cloud and digital transformation, IoT and blockchain, AI and IoT and big data analytics and so forth; it is all connected, and that’s just the meta level where IT evolutions revolve around higher degrees of interconnectedness.

The common link as per usual is and remains data, turned into intelligence and actions for the proper reasons – optimization, innovation, you name it, as long as it makes sense. With, for instance, IoT we get more data than ever. Add the explosion of other unstructured data and data which were sitting in silos for ever and now get used for a purpose. An example we mentioned previously: life sciences and pharma where you can also add hospital data and genetic data (and that’s a lot of data).

Yet, at the same time we also have a bunch of data that is never used today, also in IoT. Why? Because only a fraction fits in the scope of the IoT projects. So, we have silos, dark data and even more silos and we try to connect them all, even if we haven’t really connected the silos of data as we have had them before the IoT data deluge yet.

Silos and underutilized data are of course nothing new. With IoT being an important factor for the next steps in this inter-connected reality there are still so many IoT data challenges to be solved. That’s why blockchain, IoT data exchange models and so forth are looked at and organizations are urged to do more with the data they have which can then serve higher value generation when properly used in a clear, secure and contractually sound context as is, for instance, offered by the Industrial Data Space.

If you look at the main information technology evolutions, also in the scope of the IDC FutureScape 2018 IT predictions, essentially what you see is an industry whereby connecting all the unconnected dots, including all those data silos, still is a major task. Gateways, interfaces, APIs, the openness and agility of systems as compared to legacy systems, nuggets of software and interfaces, you name it: what we are doing is – finally – starting to build bridges on the technological level in the deepest possible sense in order to achieve the goals for which we need to build bridges on the levels of data and information, insights and actions, strategy and ecosystems of value.

All the rest is indeed about interoperability and creating digital business value and valuable services in whatever scope and in increasingly open ecosystems for those who are a bit further ahead and start getting their data act together. Although you might not see it that way the latter is one of the benefits of the GDPR in the EU by the way. Unfortunately many still haven’t started to look at it or to look at how it can benefit them from a ‘get your data together’ perspective.

What all this talk about data and silos has to do with the IDC FutureScape 2018 IT predictions and the so-called first chapter of the third platform era will become clear soon.

The quest for ubiquitous interoperability in IT and beyond

Let’s first talk a bit more about data, the role it plays and connecting the dots to turn data into actionable intelligence, scalable, value and autonomy where we will encounter the second chapter of that third platform era and even the third – future – chapter of autonomy.

Generating, aggregating and enriching data for a purpose and ecosystems, among others, means artificial intelligence, IoT and edge computing, the deployment of data-as-a-service models as we clearly see in IoT, hybrid cloud (workload per workload), more diversified types of cloud for specific purposes (and industry clouds), next gen ‘intelligent’ networks and security, containers and APIs, loads of APIs.

But don’t just think edge and IoT, think ubiquity: connecting technological dots and interoperability is happening on all levels, at the edge, between information and data management platforms, between IT and OT, between various blockchain solutions (the main blockchain solution concern as mentioned in our article on the future of blockchain) and so on. Call what organizations are doing or start doing a quest for ubiquitous interoperability and connectivity that enables to finally push through to the more mature levels of digital transformation.

It all seems so logical but often remains misunderstood. There are goals, challenges and opportunities, then there are technologies and ecosystems to achieve these goals, tackle those challenges or tap into those opportunities and, next, there are combinations and connections of technologies, data, processes and so forth that enable all of this on the level of each individual organization and on the level of ecosystems. We recommend you to read (also between the lines of) that mentioned digital transformation 2018 kick-off article. And we also recommended you to read our article on IoT in 2018 where, using our favorite term ‘holistic’ again, we call to talk less about the technology and even redefine IoT from the what to the why perspective (and the intersection of IoT and other technologies).

Interoperability and connecting the dots with information technology evolutions for ‘multiplied innovation’

If you’re still reading you maybe wonder when the heck you’re going to read about those – according to us – key takeaways from the IDC FutureScape 2018 IT predictions.

Well, for starters we already mentioned some key takeaways. However, again for us, the main takeaway has to do with the larger picture and backdrop against which IDC makes those predictions and everything we wrote so far.

Before IDC’s Frank Gens started mentioning any prediction in the ‘IDC FutureScape: Worldwide IT Industry 2018 Predictions‘ webcast, he started to explain why the company picked the ten IT predictions it did in the scope of the DX economy and covered the broad themes that had led to these predictions.

And it’s exactly here where, in our view, the key takeaway lies. Gens stated that we needed to look at the predictions against the backdrop of shifts in the third platform. As a reminder: that third platform and the innovation accelerators all are technologies (or rather: sets of technologies) that enable digital transformation.

Frank Gens started by saying that in the first years of the ‘third platform era’ world companies took a rather siloed approach and leveraged cloud, mobile and so forth to create solutions in a way we did in the client-server world.

He called that stage the first chapter of the third platform era, summarized in one word: experimentation (and do remember ‘silos’). That chapter, which more or less started in 2007 lasted until 2015-2016 for some and later for others. De facto most organizations are still in that first chapter, it’s the essence of many points made above.

It’s the first time we heard IDC talk about what it calls three chapters in the third platform technology world. Sure, in recent years the company did talk about innovation shifting to the core of digital transformation (hence also all those innovation accelerators) but three chapters, that was new.

Today (and for some sooner) we are shifting to the second chapter of that third platform era Gens said, which, summarized in two words is the stage of ‘multiplied innovation’, the core message of the IDC FutureScape 2018 IT (industry) predictions.

Future technology evolutions: autonomy, intelligence and the third chapter of the third platform era

Before we enter the fourth platform we have a third chapter that awaits us, starting somewhere roundabout 2022 and, summarized in one word, the stage of autonomy. Guess what that will be about.

If you’re looking at how in Industry 4.0, in Logistics 4.0 and even in building management and in power and energy management we’re already starting to move towards autonomous and semi-autonomous decisions by machines, IoT devices, sensors, actuators and so forth and all the technology and moving of intelligence to the edge you can do an educated guess.

Of course, autonomy will be about more than that but it’s bringing us pretty close to both the fourth platform and the digital era with even more advanced technologies (among others through the cross-fertilization of combined technologies, leading to others), more capabilities and more connected data as autonomy means decisions and decisions by systems, intelligent networks, devices and all the rest can only happen when there is intelligence (and we don’t mean human intelligence but the intelligence that is required for systems or devices to take decisions, although there will always be human decisions). To obtain that intelligence you need IoT why by definition starts at the edge and you need all the other types of data in an aggregated way (including a lot of that unused data), turned into actionable intelligence.

It’s also crystal clear that the evolutions from the ‘multiplied innovation’ stage to the third chapter, autonomy, will not just happen in a technological context but will lead to even more ethical debates, regulations, security questions, data ownership issues, privacy debates and discussion about the next levels of artificial intelligence and robotics than already is the case today, certainly when we increasingly start leveraging autonomy within the human body and mind as the future of healthcare and the fourth platform is about (but not just the future of healthcare).

FutureScape 2018 information technology evolutions: the second third platform chapter

Anyway, we leave that third chapter for what it is and, as in all honest only could listen a few minutes to the webcast and don’t know if it was even tackled, and return to that chapter we’re shifting towards in the third platform now, multiplied innovation, as it’s in that scope that the main IDC FutureScape 2018 IT industry predictions need to be seen.

However, let it be clear that this is probably the main takeaway: the days of silos are over for those who want to truly innovate. Yet, regardless of those IT predictions we all know that there are not, not in data, not in infrastructure and systems, not in the ways we work, manage, lead and transform, not in the way we service our customers or take care of the end-to-end customer experience. There are of course the often mentioned exceptions of which some will take the lead and in several industries and areas of innovation and transformation there are ever more ecosystems but, still, there is still a long way to go for those who want to go it.

All this of course doesn’t mean that the worldwide IT industry predictions make no sense, well on the contrary, they fit in that shift to this second chapter of the third platform technology world. Yet, that shift is only happening now for many and hasn’t started to happen at all for many more.

So, finally those IDC FutureScape 2018 IT industry predictions and IT evolutions in the second chapter of multiplied innovation for the DX economy: the shift towards that second chapter is, among others enabled by 1) platforms and developers, 2) open API based ecosystems of innovation, 3) hyperagile application deployment technologies (e.g containers and serverless computing), 4) an increasingly diversifying cloud ecosystem, 5) richer AI services, 6) data exchange and monetization at scale, 7) evolutions in human/digital interfaces and 8) a slowly but steadily role for blockchain as an enabler of the digital trust which is needed to power it all.

The consequence and purpose at the same time: accelerated or multiplied innovation, “digitally-enhanced offerings’, ecosystems of innovation and the next steps in digital transformation journeys for organizations that are ready for them and for the end of silos.

You can read more about all those IDC FutureScape 2018 IT (industry) predictions (and more, as there are 10 in total) in the press release from IDC and in the quotes and illustration (which shows the key IT evolutions and an interpreted adaptation of the 3 chapters of the third platform as enablers of digital transformation) in this article.

We do hope, however, that the key takeaways, beyond the technological dimensions, make as much sense to you as they do to us: simply said it’s still about connecting the dots, solving the silo and unused data issues and moving towards the next stages of digital transformation which always were and have been about genuine transformation and innovation at scale, including an ecosystem approach. But: to get there you need to be ready.

More IT industry forecasts: IT spending, hiring priorities, uncertainties and data

In January 2018 also CompTIA came with its annual IT industry outlook. CompTIA points out that, as much as there is excitement for what is coming our way and becoming reality, there are also quite some concerns and questions that increasingly become part of the mix when looking ahead.

And it’s not just for the IT industry but about organizations overall. How else could it be? One is connected with the other.

An IT industry year with many uncertainties

The Global Forensic Data Analytics Survey 2018, for instance, clearly indicates how data protection and data privacy compliance are seen as the major growing concern (think, among others, indeed GDPR again). Moreover, cyber breaches and other IT-related risks and concerns rank high too.

These factors can’t be ignored and do impact the IT industry. And there are more: geo-political uncertainties (e.g. Brexit), a potential recession, currency exchange rates being quite unstable to say the least, more regulations, less trust, a higher demand for security and transparency, you name it.

Risk and uncertainties play everywhere. Take the Deloitte Industry 4.0 executive survey, for instance. Although strictly speaking we’re in the converging landscape of IT and OT here, it’s clear that executives overall see both opportunity and risk here as well.

CompTIA also mentions a changing environment which is the backdrop against which to see the trends in the IT industry and technology evolutions. It’s a backdrop of higher expectations with regards to “business value, security, transparency and equal access to opportunity”.

The IT industry and IT spending 2018 in numbers

It does correspond a lot with what we’ve covered so far. CompTIA’s IT Industry Business Confidence Index nevertheless reached one of its highest ratings ever at the start of 2018.

It points to IDC’s technology forecasts for data on the IT industry and technology outlook 2018 but, as you can see in its IT Industry Outlook 2018 SlideShare presentation below it also sums up 12 trends to watch in 2018 that kind of summarize several of the mentioned and other evolutions we see happening. Moreover, the survey zooms in on the US, Canada and the UK with a focus on the plans of IT firms, factors that might drive or inhibit growth in 2018 and the need for skills and hiring priorities and challenges in the IT industry.

CompTIA cites data from IDC that point to a global IT industry reaching roundabout $4.8 Trillion in 2018 after having passed the $4.5 Trillion mark in 2017.

However, that seems to be on the high side and might be due to confusions regarding IT and technlogy spending. In February 2018 IDC forecasted that worldwide spending on information AND communications technology (ICT) will be nearly $4.0 Trillion in 2018. Worldwide SMB IT spending is expected to pass $600 Billion in 2018 as you can read here.

Gartner expects global IT spending to reach $3.7 Trillion in 2018. Anyway, regardless pf the exact data, also Gartner points out uncertainty factors, namely the possible impact of Brexit, currency fluctuations and a possible global recession as you can read here.

Top image: Shutterstock – Copyright: Urupong Phunkoed – All other images are the property of their respective mentioned owners.