With a clear focus on the customer experience and new – digital – ways of doing marketing, retail banks have made a significant shift to digitalization or digital transformation. Yet, the innovations mainly revolve around the front end, while the back end often remains overlooked.

It’s a crucial reason why real digital transformation in retail banks throughout departments, processes, applications, data silos and systems has been lagging behind.

Most customer-facing and front-end changes in retail banks concern gaining a single customer view, connecting omnichannel banking experiences with CRM and using customer interaction systems on the digital marketing front, including marketing automation.

These changes reflect how retail banks respond to the changing behavior and demands of digital-savyy and demanding prosumers who want to be serviced on their terms and gain access to information and assistance, regardless of channel, time, place and device.

The graphic, from a somewhat older A.T. Kearney retail banking article, shows how this central place of the modern consumer also affects the evolution of the retail bank branch.

Gaining a single customer view in order to offer better experiences is a good thing. It helps increasing sales, whether it’s through acquisition or up-selling and cross-selling. It also improves customer satisfaction and helps reducing costs.

Overlooking the back office: costs and consequences

However, when the back end is left out of the acquisition, these benefits can quickly be lost. In that sense, retail banks still have some catching up to do beyond the front office to deliver upon their promises of great customer experiences in an increasingly digital context.

Capgemini Consulting summarized these challenges well in a paper, “Backing up the Digital Front: Digitizing the Banking Back Office“.

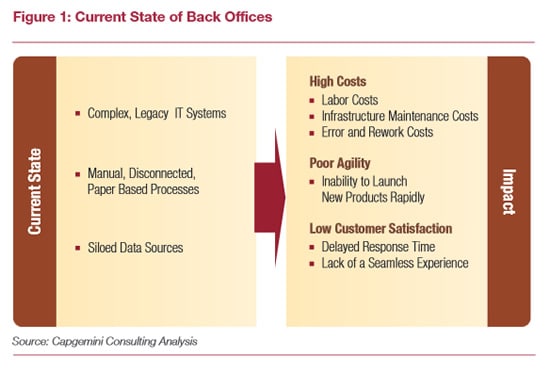

I quote: “most banks have been focusing on transforming the customer experience using digital technologies. In doing so, they are missing a potentially bigger opportunity that they have, right in their backyard – the digitization of their operations”. Although there has been progress, the Capgemini Consulting paper captures the state of back offices as it still often exists in the graphic below.

The consequences on customer satisfaction indicate how the efforts to optimize the customer experience are negatively impacted by the state of the back-office.

At least as important, is the impact on costs and agility, two of several reasons why the focus has been on digital marketing, digital customer-facing initiatives and improving customer experience to begin with:

- High labor costs (manual).

- Error and rework costs.

- Indirectly: decreased impact of overall customer experience investments.

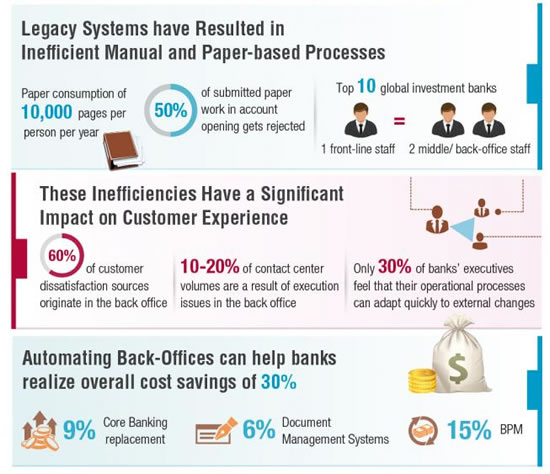

The latter is all the more apparent when looking at the infographic below regarding the impact of inefficiencies on customer experience:

- 60% of customer dissatisfaction sources originate in the back-office.

- 10 – 20% of contact center volumes are a result of execution issues in the back-office.

And of course, legacy systems, siloed data sources and manual and disconnected paper-based processes also come with higher direct costs and a poor ability to respond fast to change and develop new offerings or better adapted personal service.

So, while digital and mobile are priorities everywhere, including the retail bank branch, digital transformation at the same time is being slowed by digitalization hurdles in the back-office.

The customer experience is and remains a journey

In July 2014, McKinsey’s Tunde Olanrewaju wrote that across Europe, retail banks digitized only 20 to 40% of their processes. He warns that digital laggards, who don’t speed up their digitization efforts, the very first step in digitalization or digital transformation, will be left exposed.

Consumers simply want an end-to-end omnichannel and increasingly digital experience. The customer experience is a journey and doesn’t end at the first touch or a single “positive” interaction via a digital tool, form or application.

Furthermore, the financial impact of missing overall digital transformation opportunities – and musts – is huge.

McKinsey estimates that (quote) “digital transformation will put upward of 30 percent of a typical European bank in play, particularly in high-turnover products”. And then there is this: “banks can remove 20 to 25 percent of their cost base by leveraging (the) digital shift to transform how they process and service”.

Retail banking priorities to focus on

As always, there is a difference between the ‘best in class’ and the laggards and there are geographical (and other) differences. However, when we combine what we often still notice with the two mentioned sources, some of the back-office priorities to focus on are:

- Moving from paper to digital. In many banks and regions, paper still dominates. Capgemini Consulting reminds us in the earlier mentioned paper that back-office operations are still overly reliant on paper and manual processes.

- Making sure the customer experience is indeed looked upon as a connected journey, taking into account the cost of NOT offering the connected conditions for an overall customer experience journey approach by identifying all back-office bottlenecks and removing them.

- Reducing errors regarding data and information. This goes hand in hand with the move from paper to digital. And it’s not just about, for instance, loan applications. In several regions making payments still happens using paper too, to give just one example.

- Creating the conditions to be more agile, at the very least from a customer perspective. Digitalization should not only offer a journey-based customer experience but enable customers to “do” things themselves, for instance regarding “their” data, too. Also look at the customer onboarding process.

- Mapping and improving the processes, applications and functions that are closely connected with overall goals such as cost reduction and customer experience optimization. No process stands alone, no optimization effort stands alone.

- Moving from disconnected information silos, manual processes and (expensive) legacy IT systems to connected systems, all the way from data capturing to intelligent information management, analysis, better customer service and beyond. This doesn’t have to happen overnight as McKinsey reminds us in the mentioned article. Maximizing the use of existing technology, applying lightweight technology interventions and focusing on areas where the best gains can be made, are just a few examples of a more staged approach. Digital transformation is not a holy grail: it also enables retail banks to provide the personal touch consumers still want in the areas it makes most sense by automating and optimizing all the rest.

- Doing more with the increasing volume of data and better connect workflows, information input, information silos and processes. Putting the right data at work for the right reasons starts with capturing and combining them the right way.

- Better aligning IT with the information aspect and the business goals. Reducing manual labor and processes, for instance, by better and automated data capturing and usage, reduces costs and errors so there is more room for innovation and transformation (and personal interaction where it’s desired).

- Involving the offline dimension. The role of the retail bank branch is changing. Digital technologies become increasingly important in the physical environment (and vice versa). Although many experiments have been conducted and several retail bank branches underwent changes, the real innovative changes are yet to come.

- Preparing tomorrow today. Finally, consumers have been increasingly executing tasks themselves that once were executed by banks (as is illustrated in the graphic from A.T. Kearney research below) and that trend will continue as the so-called empowered consumer wants to have more control in specific areas (and a more personal approach in others). The question is whether the (back-office) foundations to respond to these shifts and even pro-spond by enabling execution by the customer, while maintaining a relationship and offering more choice and greater customer experiences, will be there once you need them. Information management is essential in that regard.

Siloed information (and over relying on paper) is often the enemy of optimization, transformation and even the innovation required to serve customers better in a real-time economy where customers nor competitors are waiting for business to catch up with a digital transformation reality.